While the world economy is showing a slow recovery after the Covid-19 pandemic, it is estimated that China, one of the main engines of global trade and economy, will not be able to reach its annual growth targets. However, it is argued that the Chinese economy is not as bad as the numbers suggest, and even outperforms most of any other country. The zero-covid policy, the huge debt, the real estate bubble and the size of the collapsed housing market are the key concern for the recovery of the Chinese economy.

From this point of view, Ankara Center for Crisis and Policy Studies (ANKASAM) presents the views of Agathe Demarais, the Global Forecasting Director of The Economist Intelligence Unit (EIU), in order to evaluate the short, medium and long-term forecast regarding China’s economic outlook.

- It is seen that China has not been able to achieve its annual economic growth targets. How do you think the softening of Covid-19 restrictions will have an impact on the Chinese economy in the short and medium term?

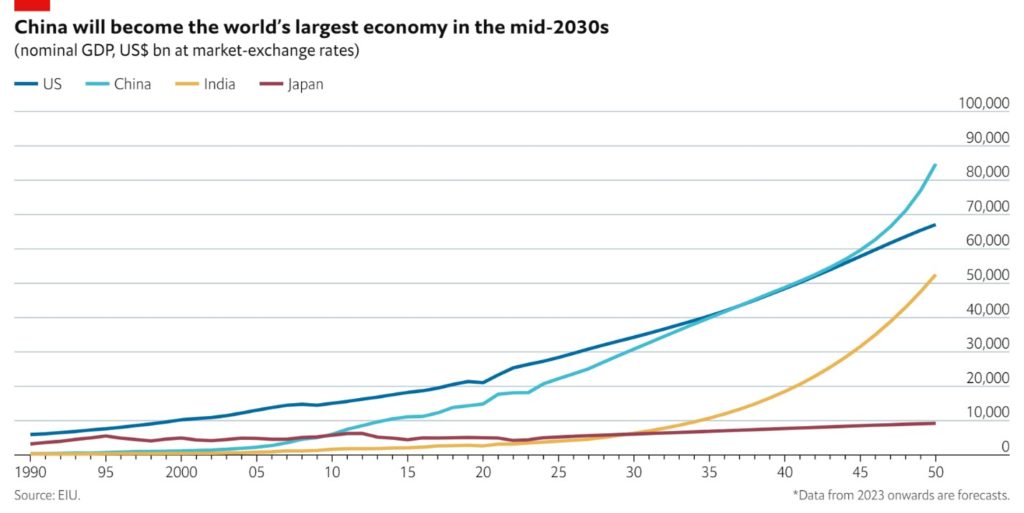

We still believe that China will become the world’s largest economy, but now believe that the crossover point will be 2037 (four years later than we previously forecast). I’ve prepared a graph highlighting our projections, which you can find below.

In the short term, the recent lifting of zero-covid restrictions will boost the prospects of the Chinese economy. We previously assumed growth of 4.7% in China next year, but will now revise this forecast upwards to 5.2% (from 4.7% previously). We will also revise our 2024 growth forecasts slightly upwards, to 4.8% (from 4.5%). It is important to note that China’s economic recovery will be different from that of western economies, where consumption recovered strongly thanks to high savings induced by ample fiscal stimulus and limited opportunities to spend during lockdowns.

China’s recovery in 2023 will be also driven by personal consumption. However, the consumption recovery will have a different path; with Chinese income growth slowing and Chinese citizens remaining cautious about Covid-19, consumption will be driven mostly by pent-up demand and low base effects tied to previous covid restrictions. This means that the spending pick-up will be milder compared with those registered in western economies, such as the US or the EU. Relatedly, even when international travel resumes, it will take at least a year for Chinese tourist flows to recover to pre-pandemic levels.

- With the current growth figures, it does not seem possible for China to surpass the US, the world’s largest economy, until 2060. What is your future provision for the Chinese economy?

In the long term, we at the EIU believe that China has mostly closed its GDP gap with the US, despite China’s poor demographic prospects. Even when the Chinese population declines, it will remain far higher than the US population. Given that population dynamics and productivity growth are the main drivers of long-term growth, this means that China’s economic supremacy will not be challenged at least until the 2060s. As you can see on the graph that I shared earlier, India may be the economy to watch afterwards – but making forecasts beyond 40 years is almost impossible.

Agathe Demarais

Agathe Demarais is the Global Forecasting Director of The Economist Intelligence Unit. Agathe is a leading voice on global issues, with a specific interest in sanctions, European affairs, Russia and the Middle East. She draws upon her extensive diplomatic experience in emerging markets, deep policy-making knowledge and her background in investment banking to help a wide variety of audiences make sense of complex developments. Agathe is also the author of Backfire, a book on the global ripple effects of sanctions (Columbia University Press, 2022). Backfire highlights the global ripple effects of sanctions on multinationals, commodity markets, and diplomatic relations. The book also analyses the impact of US controls on the exports of American semiconductor technology to China, and what these mean for the future of sanctions.